Madonna Boon

Property Manager

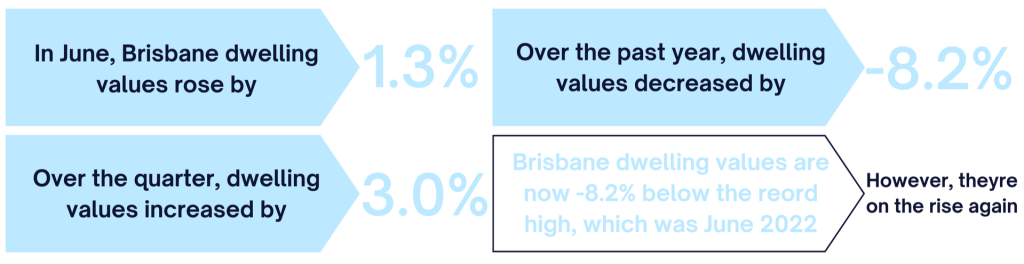

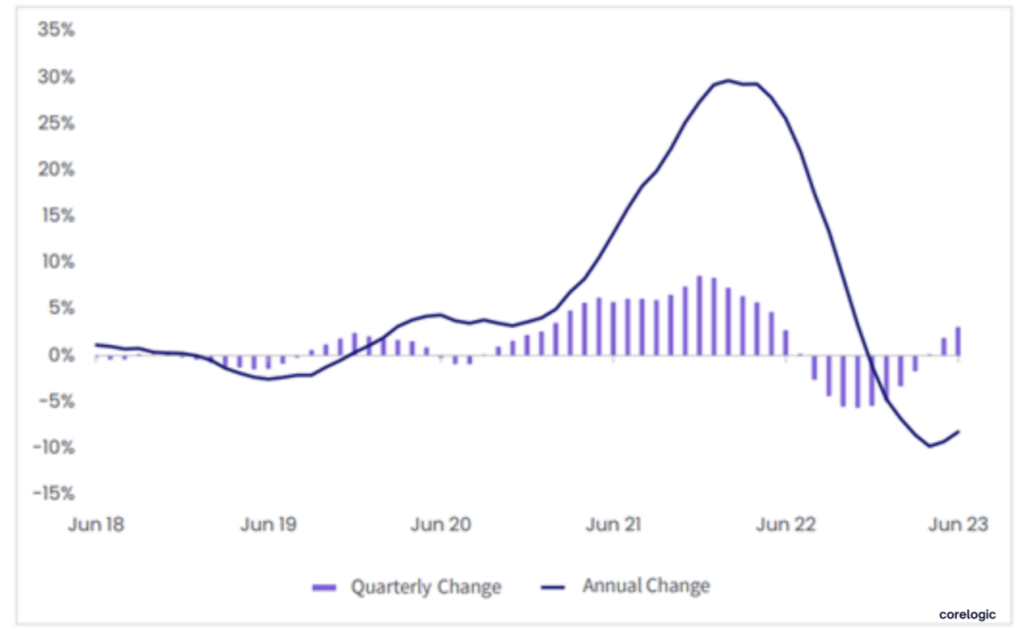

As of 2023, the Brisbane property market has passed its trough and is showing signs of stabilization. It is no longer in a boom, but it is not expected to crash either. The current situation presents an excellent opportunity for buyers and investors looking for A-grade homes or investment-grade properties in Brisbane.

Inflation seems to be under control, and interest rates are nearing their peak, which indicates a favorable environment for entering the market. The strong supply versus demand dynamics in Brisbane, coupled with interstate migration driving population growth, will likely keep property values stable and provide a solid foundation for future price increases.

While the overall economy is performing well, consumer sentiment is still influenced by negative media coverage, leading some discretionary buyers and sellers to remain on the sidelines. However, strategic investors and home buyers with a long-term perspective are taking advantage of the current window of opportunity.

It’s important to note that different locations within Brisbane are performing differently, and property types such as houses and townhouses are currently more in demand than apartments. The gap between apartment and home prices is significant, and rising building costs may eventually lead to a narrowing of this gap.

In conclusion, the 2023 Brisbane property market presents a promising scenario for long-term investors and home buyers. The combination of favorable economic conditions, population growth, and demand for housing in certain areas makes it an opportune time to consider investing in the Brisbane housing market. However, as with any investment, careful research and consideration of individual market factors are essential for making informed decisions.

Investors who seize the opportunity to purchase A-grade homes or investment-grade properties in Brisbane now are likely to reap the rewards in the coming years.

The Brisbane property market has passed its bottom, entering the upturn stage of the property cycle, making it an ideal time to make strategic investments.

Several positive growth drivers are converging, creating a perfect storm for Brisbane’s house prices to continue their upward trajectory. The recent announcement of Brisbane winning the 2032 Olympic Games will fuel significant infrastructure development, economic expansion, and population growth over the next decade. This bodes well for Southeast Queensland, which will remain an attractive destination for many Australians from interstate, drawn by the region’s lifestyle, healthcare, and affordability advantages.

However, it is essential to recognize that Brisbane’s housing market is diverse, with variations based on price point, geography, and property type. Relying solely on the general Brisbane property market to drive returns may not yield the best results. Therefore, careful property selection is crucial to ensure the investment aligns with specific goals and market dynamics.

In conclusion, the current market conditions in Brisbane present a promising outlook for investors who choose wisely. By capitalizing on the positive growth drivers and selecting the right properties, investors can position themselves for long-term success and recognize the potential of their investments as the Brisbane property market continues to flourish.

Buying a property is a significant financial decision, and getting the pricing right is paramount. Universal Buyers Agents, experts in representing property buyers, have honed their skills in accurately pricing properties to secure the best deals for their clients. In this guide, we’ll delve into the top three strategies that Universal Buyers Agents employ to ensure their clients get the most value out of their property purchases.

When it comes to property pricing, the adage “knowledge is power” holds true. Universal Buyers Agents rely heavily on conducting a thorough Comparative Market Analysis (CMA) to determine a property’s fair value. This involves examining comparable sales in the property’s area and its surroundings.

However, Universal Buyers Agents take this a step further. They focus not just on any comparable properties, but on those that share similar attributes such as the number of bedrooms, bathrooms, car spaces, land size, and overall quality. This meticulous attention to detail ensures that the properties being compared are truly like-for-like, resulting in a more accurate valuation.

Here’s where their expertise shines: Universal Buyers Agents understand that both superior and inferior properties have valuable insights to offer. Superior properties help establish a ceiling price, indicating the upper limit that a property could realistically command. Meanwhile, analysing inferior properties sets a bottom-line price, helping to delineate the lowest value a property might be worth. By encompassing this range, Universal Buyers Agents create a comprehensive pricing framework that considers all potential scenarios.

Universal Buyers Agents know that a property’s true value extends beyond its aesthetic appeal. Their commitment to due diligence sets them apart. They meticulously scrutinize the fine print and delve into a property’s intricacies before advising their clients on the right price.

The presence of factors like flooding risks, easements, overlays, noise buffers, and surrounding development applications can significantly influence a property’s valuation. Universal Buyers Agents recognize that properties with these complexities will be priced differently from those without. This meticulous analysis equips them to provide clients with a well-rounded perspective on the potential challenges and opportunities associated with a property, allowing for more informed decisions.

One of the most powerful tools in the Universal Buyers Agent’s arsenal is understanding the motivations and expectations of sellers. By engaging in open dialogue, they gain insights into whether sellers have high price expectations or are more willing to meet the market.

This understanding isn’t just about gauging the initial asking price—it’s about deciphering the seller’s mindset. Are they eager to sell quickly? Are there specific reasons motivating their sale? This knowledge helps Universal Buyers Agents craft negotiation strategies that align with the seller’s disposition, potentially giving their clients an edge during negotiations.

In conclusion, Universal Buyers Agents bring a unique blend of meticulous research, due diligence, and negotiation finesse to the art of property pricing. Their holistic approach ensures that buyers are well-equipped to make informed decisions and secure properties at prices that accurately reflect their value. If you’re navigating the complex world of property purchasing, consider enlisting the expertise of a Universal Buyers Agent to guide you through the process with confidence.

When it comes to real estate investment, one of the key decisions investors face is whether to opt for short term rental or long term rental properties. Both strategies have their merits and drawbacks, and understanding the pros and cons of each can help you make an informed choice that aligns with your financial goals and risk tolerance. In this article, we’ll explore the advantages and disadvantages of both short term and long term rental investment properties.

Short term rental properties, often referred to as vacation rentals or holiday rentals, involve renting out a property for shorter durations, typically ranging from a few nights to a few weeks. These properties are often listed on platforms like Airbnb, Vrbo, and Booking.com, targeting travellers and tourists. Let’s examine the pros and cons of this investment strategy:

Long term rental properties involve leasing a property to tenants for an extended period, typically for a year or more. This traditional rental strategy has its own set of advantages and disadvantages:

The decision between short term and long term rental investment properties depends on various factors, including your financial objectives, property location, risk appetite, and management capabilities. Some investors may choose to diversify their portfolio by having a mix of both strategies. Ultimately, conducting thorough research, understanding the local market dynamics, and seeking advice from a qualified real estate professional can help you make a well-informed investment decision that aligns with your investment goals.

Key Takeaways –

Nestled in the heart of South Australia, Adelaide, a city known for its economic resilience and steady growth, has emerged as a promising destination for property investment.

The city’s property market has reached unprecedented heights, with the median house price soaring to a record $542,913 [1].

This consistent upward trend underscores the potential that Adelaide, South Australia’s cosmopolitan coastal capital city, holds for investors seeking stable and profitable opportunities.

However, like any investment, understanding the market is key to success.

This guide provides a comprehensive overview of Adelaide’s property market, highlighting its unique attributes and the importance of informed decision-making in property investment.

Whether you’re a seasoned investor or a novice exploring investment possibilities, this guide will offer valuable insights into the dynamic world of the Adelaide property market.

Adelaide’s housing market has consistently demonstrated STABILITY and growth, making it an attractive option for investors.

Historically, the city has shown a steady rise in median prices, even outperforming other major Australian cities regarding affordability and return on investment property.

The current trends in Adelaide’s housing market, including RECORD-HIGH median house prices and a robust growth rate, further underscore its potential for property investment.

Adelaide’s economy plays a significant role in shaping its housing market. The city’s economic stability, even in times of global economic stress, contributes to the resilience of its market.

Adelaide’s economy, which makes up close to 17.7% of South Australia’s economic output, is the LARGEST growth, further enhancing its appeal to investors [2].

Image Source: Realesate.com

In addition to economic stability, Adelaide’s ongoing investment in key infrastructure PROJECTS also impacts property prices.

Projects such as the $24 million upgrade to Victoria Square/Tarntanyangga and the $30 million redevelopment of Rundle Mall not only improve the city’s infrastructure but also create jobs and stimulate economic growth [3].

These developments can increase property demand in and around these areas for home buyers, potentially driving up PROPERTY VALUES and increasing the rental yield.

Investing in Adelaide’s property market offers the potential for stable returns in a growing economy. Understanding these factors can help investors make informed decisions and maximize their investment returns.

In Adelaide’s diverse property market, investors can choose from various investment types. Each type comes with its own set of BENEFITS and challenges. Here, we delve into two popular types of property investment:

A property with positive cash flow means that the property generates more income (usually from rent) than the expenses involved in owning and maintaining the property.

In simpler terms, a property is negatively geared when the expenses of owning and managing it are higher than the money it makes. This loss can be used to reduce the amount of taxable income for the owner.

Financing is a CRUCIAL aspect of any property investment. In Adelaide, investors can finance their property investments, including traditional bank loans, non-bank lenders, and private lending.

As per the Australian Prudential Regulation Authority, as of June 2021, the value of new loan commitments for housing in South Australia was $1.5 billion, indicating a strong demand for property financing [4].

However, borrowing money to invest in property comes with its own set of RISKS and rewards. On the one hand, leveraging borrowed money can potentially amplify your returns if the property appreciates in value.

On the other hand, if the property market declines, you could end up OWING MORE than the property is worth. Therefore, it’s essential for investors to carefully consider their financing options and understand the associated risks and rewards before making a decision.

Choosing the right property is a critical step in the investment process. In Adelaide’s diverse property market, investors MUST consider various factors to identify properties that align with their investment goals. Key factors to consider include:

Investors should also pay CLOSE ATTENTION to median value growth and rental yields, as these are key indicators of a property’s potential return on investment.

Median value growth can indicate the potential for capital appreciation, while rental yields can provide insight into the property’s potential to generate rental income.

We have numerous resources to assist investors in their property search and calculations, including property investment calculators and a friendly team of property investment advisors.

Utilizing these RESOURCES can help investors make informed decisions and identify properties that align with their investment strategy.

Once you’ve secured an investment property in Adelaide, the next step is to decide on the MANAGEMENT of the property. Investors typically have two options: hiring a real estate agent or managing the property themselves.

Real estate agents can handle the day-to-day operations of the property, which can be a significant advantage for many investors.

Managing the property yourself can save on agent fees and allows for direct control over all aspects of the property.

The decision between using a real estate agent or self-managing should be based on the investor’s personal circumstances, including their time availability, proximity to the property, and comfort with handling property management tasks.

In South Australia, property investors need to be aware of several taxes and duties. One of the primary taxes is STAMP DUTY, which is charged on certain documents and transactions.

The rate of Stamp Duty can be either a flat rate or an ad valorem rate (based on the value of the transaction) depending on the specific document or transaction. You can use calculators on the RevenueSA website to estimate the amount of Stamp Duty payable [5].

Another significant tax is LAND TAX, which is levied each financial year and is based on the site value of the land. The rates and thresholds for Land Tax can be found on the RevenueSA website, and they also provide a calculator to estimate your Land Tax.

It’s IMPORTANT to note that the property owner, at midnight on 30th June each year, is liable to pay the Land Tax assessed for the forthcoming financial year.

Investing in Adelaide’s property market offers a wealth of opportunities, thanks to its economic stability and diverse range of investment options.

However, it’s key to understand the various aspects of property investment, from financing and property management to tax considerations. While this guide provides a comprehensive overview, it’s always recommended to seek professional advice tailored to your specific circumstances.

With the right knowledge and guidance, you can navigate Adelaide’s property market confidently and make informed investment decisions.

Sources –

Key Takeaways –

In the dynamic world of property investment, Perth stands out as a city of opportunity.

With its globally recognised liveability, robust economic growth, and strategic government initiatives, Perth’s property market is a beacon for domestic and international investors.

The city’s property market is currently experiencing a significant upswing, driven by a combination of factors, including strong government support, a booming economy, and a growing population.

In this article, we will delve deeper into the reasons why Perth is a compelling destination for property investment, explore the different sectors of the Perth market, and provide insights into the support available for property investors.

Whether you’re a seasoned investor or just starting out, this guide will equip you with the knowledge to make informed decisions about Perth property investment.

Perth’s property market is a vibrant ecosystem that offers a wealth of opportunities for investors. From the ambitious Perth City Deal to the city’s effective management of the COVID-19 pandemic, various factors make Perth an ATTRACTIVE destination for property investment.

The Perth City Deal is a plan worth $1.5 billion announced by the Australian & Western Australian Governments and the City of Perth. It aims to transform the city’s landscape and reflects its vision for the future. [1].

The goal of the agreement is to enhance Perth’s CBD university campuses , create a thorough CBD Transport Plan, and launch a range of infrastructure projects that capitalize on Perth’s historical, natural, and cultural assets. [2].

Image: CBD Transport Plan

The COVID-19 pandemic has had a profound impact on global property markets. However, Perth’s strong CRISIS MANAGEMENT has resulted in some unique outcomes.

Perth’s effective handling of the COVID-19 pandemic has had a positive influence on the city’s property market. Due to effective management and increased migration, the residential vacancy rate has reached a historic low that has not been seen in 40 years.

Investors now have new opportunities to invest in property asset classes in Perth, making it a great time to consider investing.

Due to the pandemic, more people are considering a move to Perth, causing a surge in demand for residential properties. As a result, there is a historically low vacancy rate. This trend, of course, creates new opportunities for investors, particularly in the residential property sector.

Perth’s projected population growth is another key driver of property investment in the city.

Perth’s population is expected to hit a projected 3.5 million by 2050, making it Australia’s third-largest capital [3]. This significant growth is set to fuel investment in property by PUBLIC and PRIVATE investors, making it an exciting time to consider property investment in Perth.

The projected population growth in Perth is fuelling significant investment in property. As the city grows, so does the demand for residential and commercial properties. This INCREASED DEMAND presents a great opportunity for investors to capitalise on Perth’s growth trajectory.

Project 90K is a visionary initiative commissioned by the Property Council of Australia. The project aims to more than DOUBLE the residential population within the City of Perth boundary by 2050, bringing the total to 90,000 residents [4].

This ambitious plan is set to transform the city’s landscape, creating a vibrant, bustling metropolis that offers a high quality of life for its residents.

An increase of nearly 90,000 residents in the City of Perth will lead to higher demand for different facilities and services.

This includes the need for additional:

The growing population is expected to drive demand for commercial properties, making it a great opportunity for investors interested in this sector. This includes retail spaces and office buildings, among other property types.

Perth’s commercial property market is a DYNAMIC BLEND of traditional office spaces and innovative co-working solutions. Here are some compelling reasons to consider Perth for your next commercial property investment:

Perth’s Central Business District (CBD) is a bustling centre of commerce and industry. It’s not just the city’s heart but also a prime location for commercial property investment [5].

The traditional office space model is being challenged by the rise of co-working/serviced office space providers. These flexible workspaces are becoming increasingly popular, especially among startups and small businesses.

These factors, combined with Perth’s strong economy and high liveability, make it an attractive destination for commercial property investment.

Perth’s residential property market is a blend of affordability, high rental yields, and low vacancy rates. Here are some compelling reasons to consider Perth for your next residential property investment:

Perth’s residential property market offers a unique mix of affordability and strong demand, making it an attractive option for investors.

Perth’s residential property market offers attractive yields, outpacing other major Australian cities.

These factors, combined with Perth’s high liveability and strong population projected growth, make it an attractive destination for residential property investment.

Perth stands out as a compelling choice for property investment. Its property market, marked by affordability, low vacancy rates, and high rental yields, offers unique opportunities for residential and commercial investors.

The city’s high liveability and significant economic investment further enhance its appeal. Whether you’re an experienced investor or a beginner, Perth’s dynamic property market and robust economy make it an ideal location for your next investment.

Sources –

Key Takeaways –

Welcome to our comprehensive guide on leveraging your superannuation to climb the property ladder. As you navigate the complex world of home buying in Australia, you might ask, ‘Can I use my super to buy a house?’

The answer is yes; certain schemes and strategies allow you to tap into your superannuation to fund your home purchase, making the dream of homeownership more attainable.

Superannuation, a long-term savings arrangement designed to provide income in retirement, is more than just a retirement fund. It can be a powerful tool in your home-buying journey.

With careful planning and a thorough understanding of the rules, you can use your super to buy a home, turning this long-term investment into a stepping stone towards your first property.

In this guide, we will delve into the intricacies of using super to buy a house, focusing on the First Home Super Saver Scheme and the Self-managed Super Fund.

We will also explore other alternatives for home buying, helping you make an informed decision that aligns with your financial goals.

Whether you’re a first-time home buyer or considering your options, this guide will provide you with the essential knowledge to navigate the Australian property market with confidence. Let’s embark on this journey together, turning the dream of homeownership into a reality.

Superannuation, often called ‘super’, is a compulsory LONG-TERM savings scheme in Australia designed to provide individuals with a source of income during their retirement years. It is a way to ensure Australians have enough funds to support themselves after they stop working.

Employers are required by law to contribute to their employees’ super fund, which is then invested on behalf of the employee. The goal is to GROW these funds over the course of an individual’s working life, providing a nest egg for retirement.

But the question often arises, ‘Can I use my super to buy a house?’ While the primary purpose of superannuation is to provide income in RETIREMENT, there are certain circumstances where you can access your super early.

One such circumstance is the First Home Super Saver (FHSS) scheme, which allows individuals to save for their first home inside their fund [1]. This scheme can be a beneficial way to FAST-TRACK your savings for a home deposit, thanks to the concessional tax treatment of super.

In the following sections, we will delve deeper into how to use your super for an investment property, focusing on the FHSS scheme and the Self-managed Super Fund (SMSF) [2].

Understanding these options can provide a significant boost in your journey towards homeownership.

The First Home Super Saver (FHSS) scheme is a government initiative that allows individuals to save for their first home inside their super account fund. This scheme leverages the concessional tax treatment of super to help fast-track your savings.

To be eligible for the FHSS scheme, individuals must meet the following criteria:

Applying for the FHSS involves the following steps:

Like any financial decision, using the FHSS scheme has pros and cons.

Pros:

Cons:

The FHSS scheme offers significant tax advantages that can help you save for your first home faster. Here are the key tax benefits:

A Self-managed Super Fund (SMSF) is a private superannuation fund you manage yourself. SMSFs differ from regular super funds and are regulated by the (ATO).

While it’s generally not possible to access your super until you retire, there are certain circumstances where you can use your SMSF to buy a property. However, the property must meet certain CONDITIONS, and the purchase must comply with the laws and regulations for SMSFs.

There are strict rules and restrictions when using an SMSF to buy a property:

Understanding these rules is crucial to ensure your SMSF property loan stays compliant and you avoid penalties.

If using your super to buy a home doesn’t work for you, there are several other options available. Let’s explore some of these alternatives.

A guarantor loan is a home loan where a third party (usually a family member) agrees to be RESPONSIBLE for your loan if you can’t make the repayments.

Pros:

Cons:

LMI is a type of insurance that protects the lender if you default on your home loan. It’s typically required if you borrow more than 80% of the property’s value.

The FHBG scheme is a government initiative that allows eligible first-home buyers to purchase a home with a deposit as low as 5%, with the government guaranteeing up to 15% of the loan [4].

The Deposit Boost Loan is a type of loan that provides a boost to your home deposit, making it easier to buy a home sooner [5].

The decision to use your superannuation to fund a house deposit is a significant one. Here are some key points to consider:

Before deciding, it’s crucial to weigh these factors and consider seeking professional financial advice.

The percentage of super you can withdraw depends on the specific circumstances under which you are accessing your super.

For instance, under the First Home Super Saver Scheme, you can apply to have a MAXIMUM of $15,000 of your voluntary contributions from any one financial year included in your eligible contributions to be released, up to a total of $30,000 contributions across all years.

You can access your super tax-free when you reach the age of 60 and meet a condition of release, such as retiring from the workforce.

If you access your super before the age of 60, you may be required to pay tax on the withdrawal, depending on the components of your super.

The time it takes to release super for a house deposit can vary. Once you apply to the (ATO) to release your super under the First Home Super Saver Scheme, it typically takes around 15 to 25 business days for the ATO to process the request and for the money to be paid.

Generally, being unemployed does NOT grant you the right to access your super early to buy a house. However, if you’re experiencing severe financial hardship or specific compassionate grounds, you might be able to access a portion of your super.

Note that these are assessed case-by-case, and strict eligibility criteria apply.

If you’re a temporary resident in Australia on a visa, you generally CANNOT access your super until you leave Australia permanently.

There are some EXCEPTIONS, such as if you have a temporary resident visa and you’re suffering from a terminal medical condition or severe financial hardship. As the rules can be complex, it’s recommended to seek professional advice.

Currently, the concessional contributions cap is $27,500 for all individuals, regardless of age. This cap is indexed in line with AVERAGE weekly ordinary time earnings but will only increase in increments of $2,500.

It’s important to note that if you exceed the cap, you may have to pay EXTRA. Also, the rules around superannuation contributions can change, so it’s always a good idea to check the current rules with the Australian Taxation Office or a financial advisor.

In conclusion, using your super to buy a home can be a great way to achieve homeownership faster. However, consider the pros and cons before making this decision.

Make sure you understand all the rules and regulations associated with accessing your super early, as well as any potential tax implications.

Sources –

Property Manager

Buyers Agent

Business Development Manager

Buyers Agent

Searcher and Sourcer

Buyers Agent

Searcher and Sourcer – Team Piper

Buyers Agent

Senior Property Manager

Client Concierge

Associate

Buyers Agent